Quantitative Easing vs. Tightening: How Central Banks Control Your Money

Central banks act as the “engineers” of the financial system, using two primary levers to steer the economy: Quantitative Easing (QE) and Quantitative Tightening (QT). While standard interest rate adjustments focus on the “price” of money, these tools focus on the “quantity” of money flowing through the banking system.

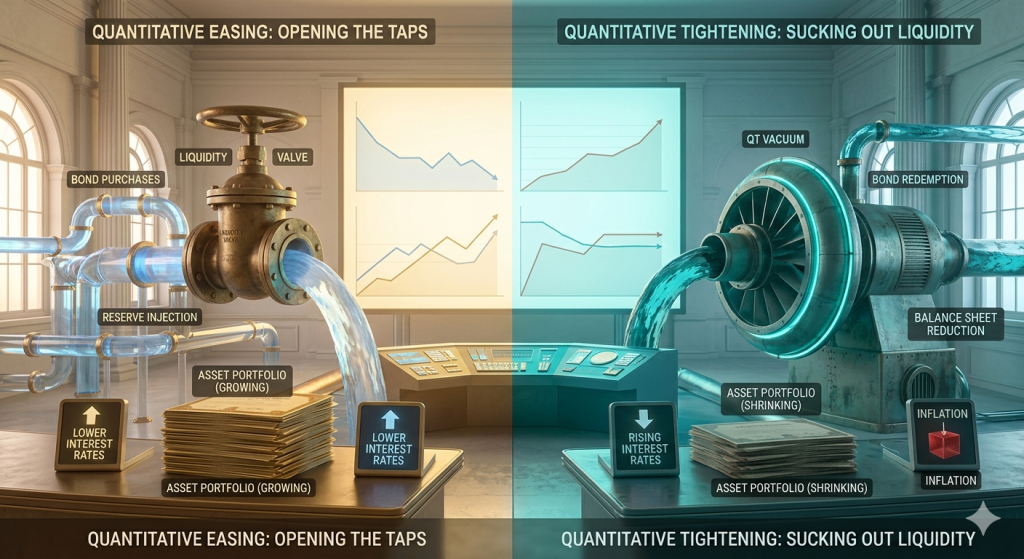

1. Quantitative Easing: “Opening the Taps”

Quantitative Easing (QE) is an unconventional monetary policy used when traditional tools like lowering short-term interest rates fail to spur growth.

- The Mechanism: The central bank creates digital money to purchase large quantities of financial assets, such as government bonds, from private banks.

- The Goal: By buying these bonds, the central bank pushes bond prices up and effectively drives down long-term interest rates.

- The Economic Impact: Lower rates make it cheaper for businesses to expand and for consumers to take out mortgages. The Liquidity Boost: The money used for these purchases increases reserves in the banking sector, encouraging banks to lend more freely. Learn more

2. Quantitative Tightening: “Sucking Out Liquidity”

Quantitative Tightening (QT) is the inverse of QE. It is typically deployed when the economy is “overheating” characterized by high inflation requiring the central bank to cool things down.

- The Mechanism: The central bank reduces its balance sheet by selling bond holdings or letting existing bonds mature without reinvesting the proceeds.

- The Goal: This removes liquidity from the financial system, causing bond prices to fall and interest rates to rise.

- The Economic Impact: Higher rates increase the cost of borrowing, which helps lower consumer spending and business investment to control inflation.

Read: The Impact of Inflation on Your Retirement Savings

3. Comparing the Impact on Your Money

| Feature | Quantitative Easing (QE) | Quantitative Tightening (QT) |

| Primary Goal | Stimulate growth | Control inflation |

| Interest Rates | Pushes long-term rates down | Pushes long-term rates up |

| Borrowing | Makes loans and mortgages cheaper | Makes loans and mortgages more expensive |

| Asset Prices | Tends to inflate stock and real estate prices | Can lead to volatility or price drops in assets |

4. Current Trends and Risks

As of early 2026, many global central banks have transitioned from massive QE programs to sustained Quantitative Tightening to battle persistent inflationary pressures.

However, these shifts carry significant risks:

- Market Volatility: Markets often react sharply to hints that liquidity is being withdrawn, which can cause spikes in bond yields.

- Liquidity Scarcity: If QT is too aggressive, it can create a “reserve scarcity” where banks lack the necessary cash for daily transactions.

- Lag Time: There is often a significant time lag between a central bank’s action and its effect on the actual economy.